Borrowers enrolled in the SAVE program confront a new era of repayment as reported changes to the federal student loan system promise higher stakes, new choices, and renewed uncertainty

By: Jerome Brookshire

A profound transformation of the federal student loan landscape is poised to affect millions of Americans in the coming months, as borrowers enrolled in the Biden-era Saving on a Valuable Education program, commonly known as SAVE, prepare to navigate a dramatically altered repayment system.

According to a report on Sunday in The New York Times, approximately 7 million borrowers currently enrolled in SAVE will soon be required to select a new repayment option for their federal student loans or risk being automatically assigned to a standard repayment structure by the federal government. The development marks the culmination of a prolonged period of uncertainty that began when Republican attorneys general challenged the SAVE program in court, effectively freezing key aspects of the initiative and leaving borrowers in a state of financial limbo for nearly 2 years.

As described by The New York Times, federal loan servicers are expected to begin contacting SAVE participants beginning July 1, providing instructions and deadlines for selecting alternative repayment arrangements. The changes emerge amid broader reforms to the federal student loan system reportedly tied to legislation enacted last year and now entering the implementation phase.

For many borrowers, the timing could hardly be more difficult.

After years of pandemic-era disruptions, repayment pauses, legal battles, and shifting federal policies, millions of Americans now face the prospect of recalculating their financial futures at a moment when inflationary pressures, rising utility costs, elevated fuel prices, and increasing health care expenses continue to strain household budgets.

“There’s a lot of anxiety out there,” Betsy Mayotte, president of The Institute of Student Loan Advisors, told The New York Times. “It’s not just about the student loan payments going up. It’s everything hitting at once.”

Her observation captures a broader reality confronting borrowers nationwide. What might once have been viewed as a routine administrative transition has become, for many families, a significant financial event with long-term implications.

The SAVE program was originally designed as one of the most generous income-driven repayment options ever offered to federal student loan borrowers. By linking monthly payments to income and household circumstances, the plan sought to reduce repayment burdens while accelerating forgiveness for some borrowers.

Now, according to The New York Times, the program is being dismantled, forcing participants to reevaluate their options.

Borrowers who fail to select a new repayment plan will reportedly be placed automatically into the existing standard repayment structure. Under that arrangement, borrowers generally make fixed monthly payments over a 10-year period, though repayment terms may be longer for consolidated loans.

Financial counselors interviewed by The New York Times have emphasized the importance of proactive decision-making.

Rather than allowing the government to assign a repayment structure automatically, experts recommend that borrowers carefully evaluate all available options and determine which program best aligns with their income, career trajectory, household obligations, and long-term financial objectives.

The consequences of making the wrong choice could reverberate for decades.

According to The New York Times, borrowers leaving SAVE will encounter a significantly revised repayment environment.

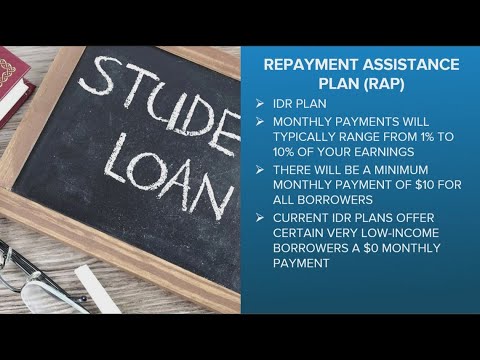

For many, the primary decision will involve choosing between the long-standing Income-Based Repayment plan, known as I.B.R., and a newly created program called the Repayment Assistance Plan, or RAP.

Under I.B.R., borrowers generally contribute a percentage of their discretionary income toward loan repayment. For loans originated on or after July 1, 2014, payments are generally calculated at 10 percent of discretionary income over a 20-year period before forgiveness eligibility is reached. Older loans may remain subject to a 15 percent formula extending over 25 years.

The New York Times reported that borrowers who do not expect to take out additional federal student loans may continue to access I.B.R., making it an attractive option for many former SAVE participants.

At the same time, federal officials are introducing RAP, a newly designed repayment model intended to replace aspects of previous income-driven programs.

While RAP shares certain philosophical similarities with earlier repayment structures, its operational framework differs considerably.

As described by The New York Times, RAP employs a graduated payment schedule based upon adjusted gross income.

Rather than shielding a portion of income before calculating payment obligations, RAP reportedly requires borrowers to contribute between 1 percent and 10 percent of their adjusted gross income, depending upon earnings.

The structure creates a more direct connection between income levels and repayment obligations. The program also extends repayment periods significantly.

According to The New York Times report, RAP may require participation for as long as 30 years before any remaining balance is forgiven. This represents a substantially longer horizon than many previous income-driven repayment programs.

RAP includes several features designed to prevent balances from spiraling upward through negative amortization.

If monthly payments fail to cover accrued interest, the excess interest is reportedly erased rather than capitalized. In addition, borrowers may benefit from provisions that ensure at least some reduction in principal balances each month.

For supporters of the program, these protections address one of the most persistent criticisms of previous repayment systems: the phenomenon of borrowers making payments for years while watching balances continue to grow.

Yet experts interviewed by The New York Times have also identified significant concerns.

One of the most notable involves inflation. Because RAP reportedly lacks inflation indexing, borrowers whose wages merely keep pace with rising prices could find themselves pushed into higher payment tiers despite experiencing no meaningful increase in purchasing power.

“For someone who has a modest income today, and whose paycheck just keeps up with inflation, they’d essentially see their monthly payment double over 20 years without really seeing a raise beyond inflation,” Rich Williams, chief customer officer at Summer, told The New York Times.

Williams further warned that the structure could create abrupt payment increases. “It’s like a step effect,” he explained.

Unlike other repayment systems that increase obligations gradually as income rises, RAP may produce sharp jumps whenever borrowers cross specified income thresholds.

For many analysts, that characteristic represents one of the program’s most controversial features.

The changes described by The New York Times are unlikely to affect all borrowers equally. Individuals with very low incomes may continue to find greater advantages within the I.B.R. framework. Under that structure, some borrowers may qualify for $0 monthly payments while continuing to accumulate progress toward eventual loan forgiveness.

Borrowers with moderate incomes and relatively manageable debt loads, however, could potentially benefit from RAP’s principal reduction provisions. For those individuals, repayment may be completed before forgiveness ever becomes necessary.

Yet determining the optimal path requires careful analysis.

Financial experts repeatedly emphasize that repayment decisions should not be based solely upon immediate monthly affordability. Instead, borrowers must consider total lifetime repayment costs, forgiveness timelines, career expectations, family circumstances, and future borrowing plans.

The complexity of those calculations has transformed student loan repayment into a sophisticated financial planning exercise.

Perhaps one of the most consequential aspects of the reported changes involves borrower mobility between programs. Historically, borrowers could often move between income-driven repayment plans without losing credit toward eventual forgiveness.

According to The New York Times, that flexibility may be significantly reduced under RAP. Abby Shafroth, managing director of advocacy at the National Consumer Law Center, highlighted the importance of understanding the implications before enrolling. “It makes it a higher-stakes decision to enroll in RAP,” Shafroth told The New York Times. “If you’re enrolling in RAP, you should generally be doing so because you think it’s going to be the best plan for you long term, not just the best plan for you right now.”

That warning reflects a broader theme emerging throughout the transition: decisions made during the coming months could shape borrowers’ financial obligations for decades.

For millions of Americans, selecting a repayment plan is no longer merely a bureaucratic exercise. It has become one of the most consequential financial choices they may make in the years ahead.

Among the groups most closely scrutinizing the reported changes are participants in the Public Service Loan Forgiveness program, commonly referred to as P.S.L.F.

According to The New York Times report, public servants—including teachers, librarians, social workers, public defenders, firefighters, law enforcement personnel, military service members, and employees of nonprofit organizations—remain eligible for loan forgiveness after making 120 qualifying monthly payments while employed in eligible public-service positions.

For these borrowers, financial advisers suggest that the central objective remains minimizing monthly payments rather than reducing total lifetime repayment costs.

Because balances can be forgiven after approximately 10 years of qualifying service, the lowest available payment often becomes the most advantageous strategy. The New York Times reported that both Income-Based Repayment and the new Repayment Assistance Plan are expected to count toward Public Service Loan Forgiveness requirements.

For many public-sector workers, therefore, the choice between I.B.R. and RAP may revolve primarily around monthly affordability rather than long-term repayment projections. Even so, experts caution that borrowers should carefully evaluate each option before enrolling.

The sheer complexity of the evolving system has led many advocates to urge borrowers to seek professional guidance before making irreversible decisions.

Another issue receiving considerable attention involves loan consolidation. Historically, consolidation has served as a useful tool for borrowers seeking simplified repayment structures or access to certain federal programs.

Yet under the framework described in The New York Times report, consolidation may now carry consequences that many borrowers fail to recognize. When borrowers consolidate federal student loans, they effectively create a new loan that pays off existing obligations.

While that process can simplify repayment administration, it may also alter eligibility for forgiveness programs and repayment plans. According to The New York Times report, borrowers who consolidate could lose existing progress accumulated toward income-driven repayment forgiveness.

Consumer advocates have expressed particular concern that many borrowers remain unaware of these implications. “That’s a big risk that few people know about,” Abby Shafroth told The New York Times.

The warning underscores a recurring theme emerging throughout the transition: actions that appear beneficial on the surface may carry significant long-term consequences. Borrowers considering consolidation are being urged to review their repayment histories carefully and understand exactly how consolidation may affect future forgiveness eligibility.

Not all borrowers face immediate deadlines. The New York Times reported that individuals currently enrolled in the Pay As You Earn program, known as PAYE, or the Income-Contingent Repayment plan, commonly called I.C.R., are not required to take immediate action. However, both programs are reportedly scheduled to be phased out by July 2028. That means participants will eventually need to transition into alternative repayment structures.

For many PAYE borrowers whose loans originated after July 1, 2014, Income-Based Repayment may offer a relatively seamless transition with similar payment calculations. Many Income-Contingent Repayment participants may even discover lower monthly obligations under I.B.R. Nevertheless, experts emphasize that borrowers should not wait until the final months before these programs close.

Early planning may provide greater flexibility and reduce the likelihood of administrative complications.

Perhaps no group faces more dramatic changes than Parent PLUS borrowers. These loans, used by parents to help finance their children’s higher education, have long occupied a distinct category within the federal student loan system.

According to The New York Times, parents who obtain new federal loans after July 1 will reportedly face a far narrower range of repayment choices than in the past. Most notably, access to income-driven repayment programs will be significantly restricted. Instead, many future Parent PLUS borrowers may be limited to the new tiered standard repayment plan.

The implications could be substantial. Income-driven repayment plans have traditionally provided an important safety net for borrowers facing financial hardship or fluctuating incomes.

Without access to those programs, some families may encounter greater difficulty managing repayment obligations during periods of economic stress.

At the same time, The New York Times reported that certain existing Parent PLUS borrowers who have already consolidated their loans may actually benefit from the new framework by gaining access to Income-Based Repayment. For those individuals, repayment costs could decline relative to previous options.

The outcome, once again, depends heavily on timing, loan history, and individual circumstances.

The student loan transition is unfolding against a broader economic backdrop that many borrowers find troubling. The New York Times noted that repayment changes are arriving at a moment when many households are already struggling with rising costs. Inflation, while lower than its peak levels, continues to influence everyday expenses. Energy costs remain volatile. Housing affordability remains a challenge in many regions. Health care expenditures continue to consume increasing portions of household budgets.

For millions of Americans, student loan payments represent only one component of a larger financial equation. Financial counselors report that borrowers increasingly view repayment decisions through the lens of overall household stability.

A repayment increase of even a few hundred dollars per month can affect savings plans, homeownership goals, retirement contributions, and family budgets. The resulting anxiety has become a recurring theme in discussions surrounding the coming transition.

Loan servicers are preparing for what could become one of the largest administrative transitions in recent federal student loan history. According to The New York Times report, industry officials expect substantial volumes of repayment-plan applications as SAVE participants evaluate their alternatives. Scott Buchanan, executive director of the Student Loan Servicing Alliance, told The New York Times that current processing times remain relatively manageable.

New applications can generally be processed within a matter of days. However, that timeline may change considerably once millions of borrowers begin submitting requests simultaneously. Borrowers who authorize automatic access to tax records are expected to experience faster processing times. Those who must provide alternative documentation because their current income differs from their most recent tax return may encounter longer review periods.

Financial advisers consistently recommend avoiding last-minute decisions. Submitting applications early may help borrowers avoid administrative backlogs and ensure uninterrupted access to preferred repayment plans.

Not every borrower will be capable of resuming payments immediately. Job losses, medical emergencies, family crises, and economic disruptions remain realities for millions of Americans.

According to The New York Times, borrowers facing financial distress will continue to have certain relief options available. Forbearance remains one of the principal mechanisms for temporarily suspending payments. Under the framework described by the newspaper, borrowers may generally pause payments for up to nine consecutive months through forbearance.

However, policymakers increasingly appear to favor longer-term repayment solutions rather than repeated temporary suspensions. The goal, according to experts cited by The New York Times, is to encourage enrollment in sustainable repayment programs rather than reliance on recurring pauses.

Certain deferment options are also expected to remain available for specific circumstances, including military service, cancer treatment, and educational enrollment.

Taken together, the reported changes represent one of the most consequential restructurings of federal student loan repayment in decades.

The SAVE program once represented the centerpiece of a broader effort to reduce repayment burdens through expansive income-driven protections.

Its dismantling signals a substantial shift in policy direction. Supporters of the new framework argue that it introduces greater accountability, clearer repayment expectations, and mechanisms designed to prevent runaway balance growth. Critics counter that longer repayment periods, inflation-related concerns, and reduced flexibility may ultimately leave some borrowers worse off.

Regardless of where the debate ultimately lands, one reality remains unmistakable. Millions of Americans are entering a period of transition that will require careful financial planning, detailed analysis, and informed decision-making.

For borrowers accustomed to years of uncertainty, the coming months will determine not only their monthly payments but potentially the trajectory of their financial lives for the next 20 to 30 years.

As The New York Times has reported, federal servicers will soon begin notifying affected borrowers, setting in motion a process that could reshape the economic outlook of millions of households across the nation. For some, the changes may create new opportunities to manage debt more effectively. For others, they may introduce higher costs and difficult choices.

What is clear is that the era of waiting is ending. The next chapter of federal student loan repayment is about to begin, and millions of borrowers will soon be forced to decide how they intend to navigate it.